Ben Munyan

Assistant Professor, FinanceVanderbilt University

Owen Graduate School of Management

Nashville, TN 37203

United States

About Me

I am an Assistant Professor of Finance at the Owen Graduate School of Management, Vanderbilt University. I research short-term funding markets and corporate bond liquidity.

Research

Working Papers and Work in Progress:Handbook of Financial Markets Chapter: The Repo Market (Edward Elger Publishing, forthcoming 2022)

The Effects of the Volcker Rule on Corporate Bond Trading: Evidence from the Underwriting Exemption

-

Regulatory Arbitrage in Repo Markets (R&R at Review of Financial Studies)

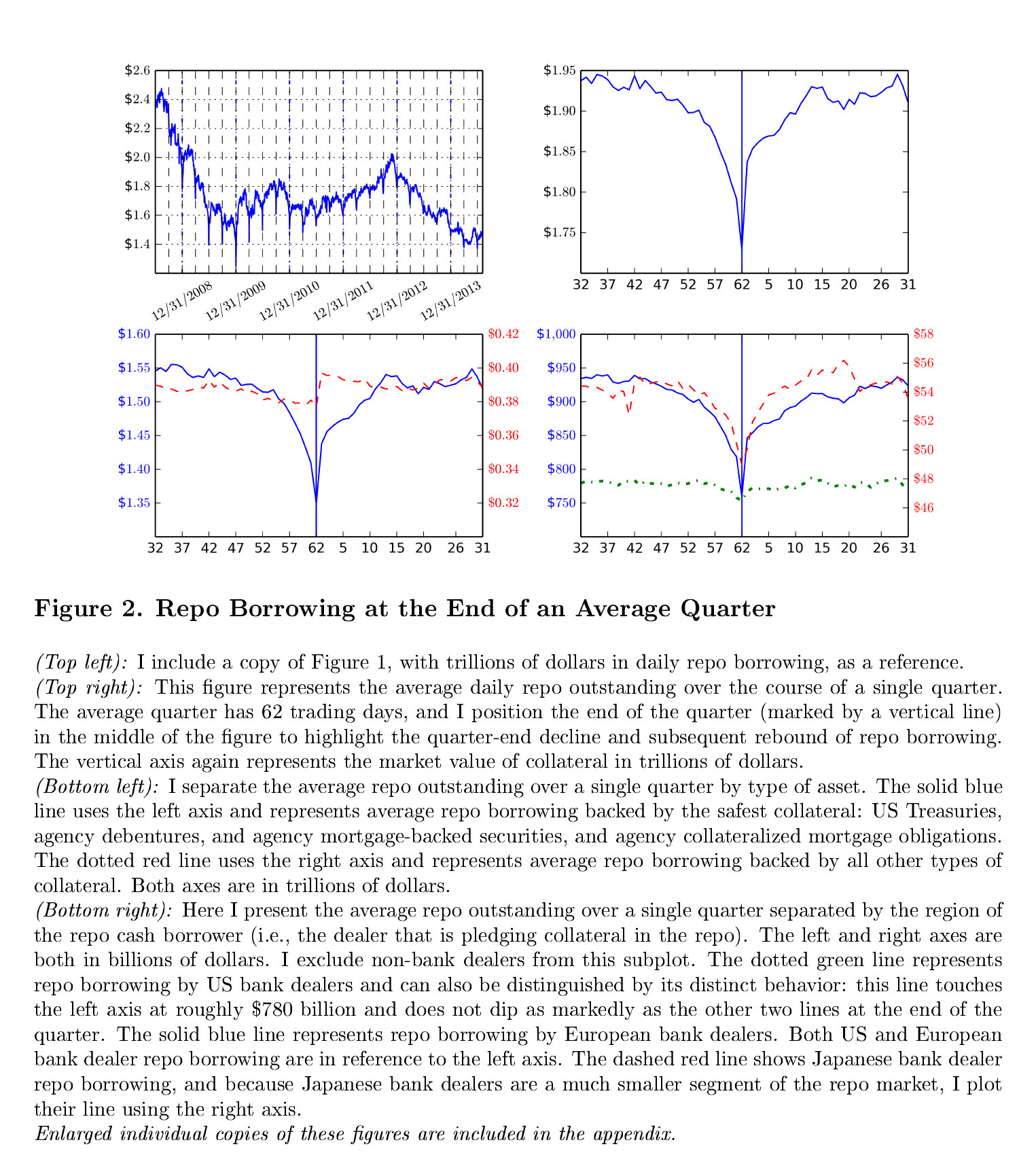

Before its collapse in September 2008, Lehman Brothers had been using the repurchase agreement (repo) market to hide up to $50 billion from their balance sheet at the end of each quarter. When this "Repo 105" scheme was uncovered (a type of strategy called window dressing), the Securities and Exchange Commission conducted an inquiry into public US financial institutions and concluded that Lehman was an isolated case. Using confidential regulatory data on daily repo transactions from July 2008 to July 2014, I show that non-US banks continue to remove an average of $170 billion from the US tri-party repo market every quarter-end. This amount is more than double the $76 billion market-wide drop in tri-party repo during the turmoil of the 2008 financial crisis and represents about 10% of the entire tri-party repo market. Window dressing induced deleveraging spills over into agency bond markets and money market funds and affects market quality each quarter, and understates balance sheet based measures of systemic risk for non-US banks.

-

Demand deposit contracts provide liquidity to investors; however by their nature they can expose the issuer to self-fulfilling runs. Existing models treat depositors as agents facing uncertain liquidity shocks, who seek to insure against that liquidity risk through use of a bank financed solely by deposits.聽Welfare-reducing bank runs then arise from the inherent difficulties depositors face in coordinating their withdrawals. This paper extends the classic model of Diamond & Dybvig (1983) to allow for a more realistic mixed capital structure where the bank's investments are partly financed by equity, and where differing incentives between shareholders and depositors are allowed to operate. I also further extend the model to allow shareholders to choose the level of risk in bank-financed projects. I compute the ex-ante probability of a bank run in consideration of the bank capital ratio, and I additionally compute the level of bank risk chosen by utility-maximizing shareholders who are disciplined by uncoordinated depositors. I find that even in the absence of bank negotiating power of the form in Diamond & Rajan (2000), banks can be welfare-improving institutions, and there exists a socially optimal level of bank capital. I consider the policies of a minimum capital requirement, deposit insurance, and suspension of convertibility, and provide guidance on creating optimal bank regulation. I show that the level of bank capital involves a tradeoff between sharing portfolio risk and sharing liquidity risk. Increased bank capital results in less risk-sharing between shareholders and depositors. The demand deposit contract disciplines the bank & its shareholders, and equity capital in effect disciplines the depositors (by making runs less likely). There is a socially optimal level of natural bank capital, even when I make no further social planner restrictions on bank portfolio choice in the model.

Market Dominance in Bond and CDS Interdealer Networks (with Sumudu Watugala)

Incentive Effects of Capital Ratio Requirements with Endogenous Recapitalization Costs

- Asset Management Incentive Problems Under Credit Rating Type Capital Requirements

Mutual Fund Flows and Securities Lending

Momentum Anomalies and Institutional Trading

Leverage and Credit Effects on Fixed Income Market Making

Published Research:

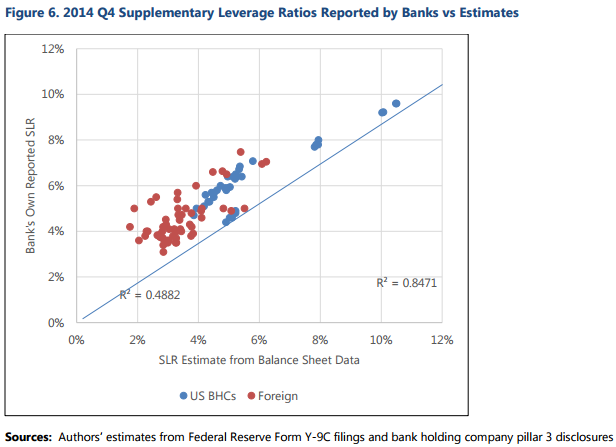

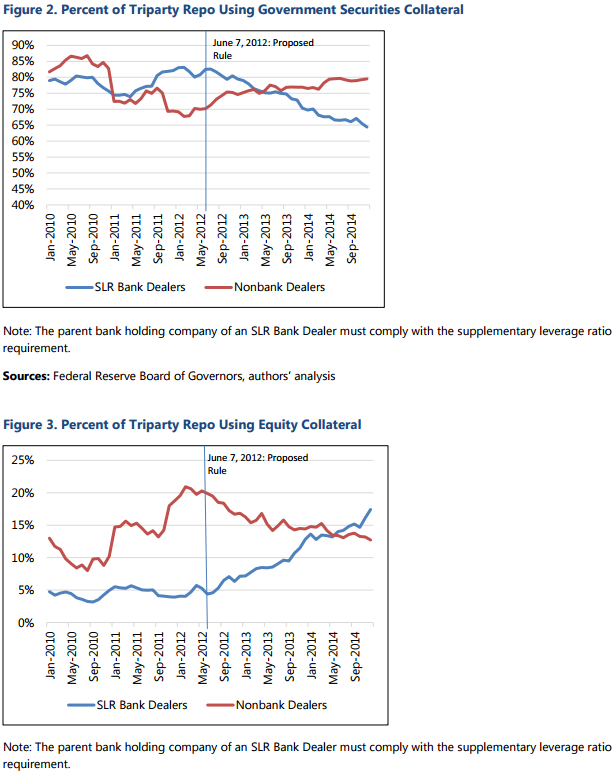

with Meraj Allahrakha and Jill Cetina -- (Journal of Financial Intermediation 2018)

While simpler than risk-based capital requirements, the leverage ratio may encourage bank risk-taking. This paper examines the activity of broker-dealers affiliated with bank holding companies (BHCs) and broker-dealers not affiliated with BHCs in the repurchase agreement (repo) market to test whether this may be occurring. Using data on the triparty repo market, the paper arrives at three findings. First, following the 2012 introduction of the supplementary leverage ratio (SLR), broker-dealer affiliates of BHCs decreased their repo borrowing but increased their use of repo backed by more price-volatile collateral. Second, the paper finds that regardless of whether a U.S. BHC-affiliated broker-dealer parent is above or below the SLR requirement, the announcement of the SLR rule has disincentivized those dealers affiliated with BHCs from borrowing in triparty repo. Finally, the paper finds an increase in the number of active nonbank-affiliated dealers in certain asset classes of triparty repo since the 2012 introduction of the supplementary leverage ratio. This suggests risks may be shifting outside the banking sector.

Research Interests

Theoretical and empirical research on financial intermediation, banking and shadow banking, government regulation, fixed-income markets, and asset management.

Teaching Experience

-

Vanderbilt University Owen Graduate School of Management:

- Instructor: MGT 6636 - Financial Institutions (2016 Mod II - Present)

- Instructor: MGT 6436 - Bond Markets (2015 Mod II - Present) University of Maryland R.H. Smith School of Business:

- Instructor: BMGT 340 - Undergraduate Corporate Finance (Spring 2013, Fall 2011)

- Teaching Assistant: BUFN 752 - Financial Restructuring, Prof. Richmond Mathews (Spring 2014)

- Teaching Assistant: BUFN 764 - Quantitative Equity Portfolio Management, Prof. Russell Wermers (Spring 2013)

- Teaching Assistant: BUFN 750 - Valuation in Corporate Finance, Prof. Dalida Kadyrzhanova (Spring 2012)

Other Interests

Technology, weightlifting, woodworking, hiking.